Empowering women with DFS

Sophie Romana and Shelley Spencer report back from the June 8 high level roundtable organized by NetHope and USAID, which brought together mobile banking and gender champions to reflect on how Digital Financial Services (“DFS”) can galvanize women’s empowerment.

Women’s empowerment is often measured by their access to resources and ability to make decisions over how they are used. Recent evidence shows that DFS delivered through mobile phones deserves solid A’s against each metric. This is not just hopeful musing by us as two empowered women with banking apps on our mobile phones. It is the consensus of a cross section of thought leaders with a seat at the table in Washington including USAID, the Bill & Melinda Gates Foundation, the Better than Cash Alliance and UNCDF, CGAP, and Women for Women International, as well as our own organizations, Oxfam and NetHope. We recently spent a morning reflecting on rigorous academic and implementation research on DFS use by women — all to be published soon — and pathways to close the gender gap in DFS product use.

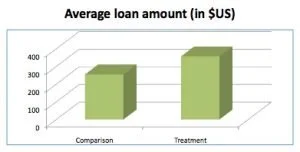

Oxfam has long known that women play a central role in financing family and community needs. What we are now finding is that DFS tools can enhance their role. To study the impact of DFS on Saving for Change (“SfC”) savings groups in Senegal, Oxfam divided up 210 SfC groups (over 5,000 women) into two cohorts: one who participated in the project and the other as a comparison set. Women who participated in the pilot saved and borrowed more than the comparison groups. The differences are not marginal. There is a significant difference in savings.

Beyond financial transactions, mastering basic operations such as making a phone call, sending a text message, and performing a transaction brought pride to these women and gave them a sense of belonging in a formal financial system.

The technology is simple, the demand is known, so why aren’t DFS more widely used by women in developing economies?

Obstacles still exist. Take a look at Women for Women International’s core empowerment program which includes education and training modules in using financial services: Efforts to use DFS were challenging in the DRC and Rwanda due to the paucity of rural mobile money agents. Furthermore, women felt that a 10 percent transaction fee was too high a cost to pay to access money they had received: They felt that accessing their own money should be free.

Increasingly there are multiple success stories from m-pesa to CARE’s Linking for Change and other popular services. Yet even with this growing body of evidence, we still don’t see massive adoption despite growing cell phone penetration rates, cheaper handsets, better technology, interest from financial institutions and mobile network operators. And the question we tried hard to answer remains – why?

What can we collectively do, as service providers, donors, private sector and civil society actors, and governments to make the promise of DFS come true for millions of underserved women in the world?

Here are some hypotheses about the kinds of actions we could take globally to unleash the feminist potential of DFS:

Can we tackle social norms that inhibit women’s participation in services (using successful approaches from other sectors be they education, health or other) and apply them to DFS to overcome resistance to women’s access to and use of DFS products? As we do with gender work, for instance, approaches could explore how to include men and women together in DFS training; or taking a leaf drawn from other training techniques by showcasing benefits to the entire family (and not the sole user) through education and awareness. Games are another avenue to make a complex product easily understandable, like the climate change games, for instance.

Will mandating use of digital payments by government (for social protection payments) or salary transfers to women mainstream DFS use and cement its value?

Can we ensure product review and adaptation are relevant to the diverse segment of women’s financial services’ needs (i.e. smallholder farmers with irregular income, garment workers with regular salaried payments). For example, factory workers and temporary economic migrants need to have access to affordable payment transfers to send money to their families at home and to save a few dollars as emergency cushions for themselves.

Will expanding the number of DFS acceptance points by including small merchants and other locations where women routinely conduct day-to-day transactions actually increase adoption of DFS? There are too few points of sale where women can use their e-wallets. Instead, most of the time, they have to transform physical cash into digital cash and then back into physical cash to be spent. They are stuck in a loop of physical cash.

Can we better analyze women’s price sensitivity of women to mobile money transaction fees, looking at the complex and diverse women market segments that may need lower transaction costs to justify use on small purchases and be more fit for purposes such as paying school fees?

How can we influence service providers to adapt their pricing schemes to create incentives for women who already are much better credit risks than men, therefore incentivizing them to become early adopters? Saving for Change has demonstrated that women members have an almost perfect repayment rate on their loans: how can we work with financial institutions so they recognize this fact and create products with better terms, instead of penalizing women with higher interest rates and collateral requirements?

We don’t know the answers yet, and it may be a combination of all the above and other factors too. What we do know is that joining forces to get the right kinds of DFS into the hands of women could have a big impact on their lives and the lives of their daughters.

This post was originally published on Oxfam’s blog. Graphs source: Saving for Change Mobile Banking, First Assessment & Learning Review, March 2016, Oxfam America