Financial access in the time of COVID-19: Self-registration for mobile money accounts in Ghana

The coronavirus pandemic is a tipping point for the digital world. As we navigate uncharted territory and practice social distancing in both the U.S. and with our team members in Ghana, Uganda, and Malawi, our thoughts turn to reaching those people without access to digital financial services.

In our work in Ghana over the past five years, we have supported expanded use of mobile money in rural areas and across agricultural value chains, and helped build the capacity of agent networks — often an essential entry point for opening a mobile money account.

Now these agent networks — and the entire Ghanian economy — are at risk. But Ghana has a model to enable easier access to mobile money and electronic payments, allowing self-registration for mobile money accounts to keep financial transactions moving. On March 18, the Bank of Ghana announced its agreement with mobile money operators to waive mobile money fees and relax KYC standards. On March 23, the Ghana Interbank Payment and Settlement Systems eliminated charges on electronic payments to further encourage the use of digital payments and slow the spread of the virus through use of cash. Other countries should follow Ghana’s lead.

In Ghana, mobile users can self-register and open accounts remotely through a short code or, in the case of AirtelTigo, by sending a “Hi” to a specific WhatsApp number. Combining the relaxation of mobile money wallet limits and waiver of mobile money fees (for money transfers between any networks for up to GHC 100 by providers) is an important approach to providing access to finance, especially in times of crisis.

AirTel/Tigo money flyers issued in Ghana

Agency banking services are adopting similar approaches to compete with mobile money services offered by mobile network operators. An example is Quick by Pan African Savings and Loans. Quick is a convenient, secured, seamless, and affordable way to access a suite of financial services on-the-go (for savings, instant loans, payments, airtime and data top ups and funds transfers) across mobile money operator wallets and agent locations. Find step-by-step instructions to sign up here.

While not using a short code, MTN customers can register for a mobile money account using a web browser or app and completing 8 steps:

Visit the MTN mobile money website

Click register

Enter your user name (which is your phone number and PIN)

Enter captcha displayed below your username

Input the one-time password sent to your phone

Create a password that you can remember, or keep the one generated for you

Repeat the password in third space and click continue

Authorize web access from your phone by dialing *126*1#

A subscriber can use the MTN Mobile Money registration app to access his/her mobile money wallet.

Other providers with similar functionalities should make an extra push to promote these products to reduce the spread of COVID-19. There is also no better or more urgent time for others to develop USSD applications, if they have the capacity to do so.

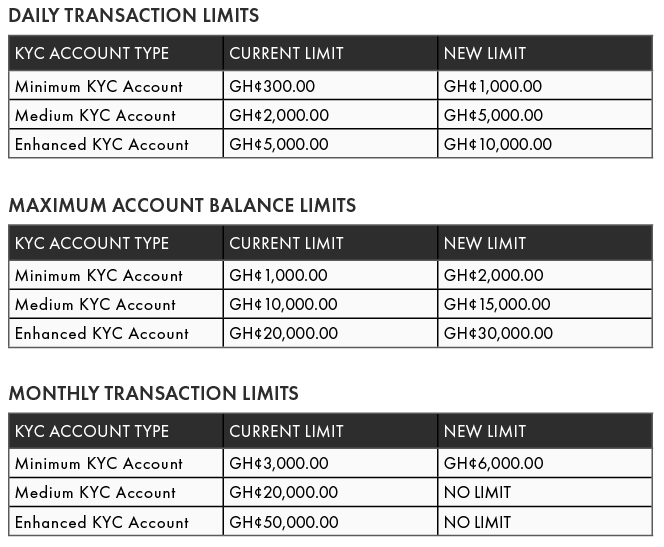

The Bank of Ghana’s new monetary policy allows mobile phone registration details to be used to open a minimum KYC account; increases the daily (by 3x) and monthly (by 2x) transaction limits on minimum KYC accounts; and doubles the permitted balance in mobile money wallets.

The collaboration of regulators, policymakers, mobile money providers, and banks in Ghana provides a roadmap for how to use digital financial solutions during the COVID-19 pandemic. The challenge now will be spreading the word on these solutions and building capacity for their use among first-time users. We stand ready and willing to take on this challenge. Developing voice messages or IVR could be suitable channels for reaching rural customers on any GSM network in the quest to self-register and perform basic financial transactions in pursuance of social distancing protocols.

In Ghana and worldwide, we call for other DFS providers to develop self-registration functionalities to promote ease and reach to new customers so that peri-urban and rural clients are not excluded in the drive toward financial inclusion.