Going cashless in the era of the coronavirus

Digital transactions are on the rise in the era of COVID-19. Using mobile money is no longer just a matter of convenience or security — it’s a matter of protecting your health.

We know the coronavirus can live on surfaces for up to 5 days, and can spread from handling a contaminated object, like paper bills, and then touching your face. Fittingly, in Uganda, we’re seeing the use of cash declining as more and more individuals are turning to contactless payment methods, like bank-to-bank transfers, cards (like VISA and UnionPay), and P2P transactions, to stay safe.

In response to the threat of the coronavirus, the Government of Uganda has curtailed movement across the country, suspending the use of all public transport (used by about 80% of the population), restricting the use of private cars, and imposing curfew hours to minimize movement and halt the spread.

These safety measures have had a significant impact on the way organizations operate, with most employees now working from home. Families are depending on formal delivery services, such as Jumia, for their daily needs, as well as informal services, like sending boda bodas (moto taxis) to pick up necessities.

Businesses that remain open, such as restaurants, supermarkets, and pharmacies, see very few walk-ins and have resorted to offering free deliveries to stay afloat. Business owners are encouraging payment via mobile money for these delivery orders in order to avoid the exchange of cash.

Boda boda delivery services encourage Ugandans to stay home.

Restaurants like Kuku Shop are resorting to free deliveries and encouraging the use of digital payments.

Meanwhile, banks are playing their part to reduce financial strain and make it as easy as possible for customers to access digital channels. Many commercial banks, like Stanbic, have temporarily reduced or eliminated usual charges to encourage use of products (like internet banking, bank to wallet, electronic fund transfers, and card payments) — optimal routes of convenience for customers who live far from their brick and mortar branches. Banks like Centenary have also increased loan limits and extended loan periods, while others have introduced new applications with location services of bank agents to help customers access their bank accounts.

In response to the current situation, Stanbic has announced the decision to update pricing of select services.

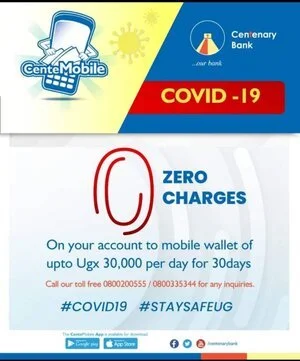

Centenary has reduced charges and revised loan limits as well.

There has already been a significant increase in the number of P2P transactions and bank-to-wallet transfers as a result of these developments. Many new customers are banking online, signing up for push and pull products and VISA cards, as well as agent banking services for access to accounts and funds.

On the downside, while MNOs would have opted to reduce withdrawal charges, the government has not given tax breaks to enable them to be able to do so. With restricted disposable income, as well, the transaction volumes on cash in at agent points has gone down, while many small businesses (deemed nonessential) continue to lose revenue by the day. And although MNOs are seeing a rise in the use of personal data, cooperative use of data has significantly gone down due to the lockdown, which has in turn affected the use of other MNO services such as mobile money. The lockdown has also disrupted the recruitment, servicing, and monitoring of agents, and there have been reports of over-charging malpractices that operators have been unable to confirm. There’s also been an increase in cases of fraud.

For as long as these circumstances last, it will be important for MNOs to provide remote support for their agents. Airtel has opened up an exclusive toll-free agent customer service line, that is offering agents support on float, sim swaps, pin resets, and other services. MNOs are also supporting the struggling restaurant business by promoting the use of mobile money to pay for their orders. MNOs should also consider increasing communications to both agents and clients about fees to avoid over-charging practices, and perhaps ramp up radio, SMS and IVR campaigns that warn customers against scammers.

Under lockdown, digital technology has provided a lifeline for families to secure necessities, and given businesses a whole new angle of cash management. While COVID-19’s long term impact on digital payments remains to be seen, it certainly has put mobile money and the many services that use it in the spotlight.